Creation of the check clearing system

The use of checks in the U.S. increased after the Civil War when federal laws passed in the 1860s discouraged banks from issuing their own paper currency (Off-site). To accommodate this shift, a complex check clearing apparatus was created to adequately distribute checks across a fragmented U.S. banking system.

However, financial institutions found check collection to be an expensive, slow process. Settling checks through the mail required an extra fee. Banks passed this cost to the check recipient, resulting in the mailed check not being paid out at its full value, known as “non-par” banking. To avoid non-par costs, banks sent checks for collection through a correspondent bank, often leading checks to circulate among multiple banks before eventually arriving at their destination.

In December 1913, President Woodrow Wilson signed the Federal Reserve Act (Off-site), which not only resulted in the creation of the Federal Reserve System but also sought to eliminate non-par banking.

Modernizing check processing abilities

Following the Federal Reserve’s establishment, the basic technology of check processing remained largely manual and time-consuming until further improvements were made in the 1940s and 1950s.

After World War II, the volume of check production increased significantly, leading the Federal Reserve to adopt new technologies and practices, including the standardization of check size and shape, implementation of routing numbers for banks, and creation of account numbers.

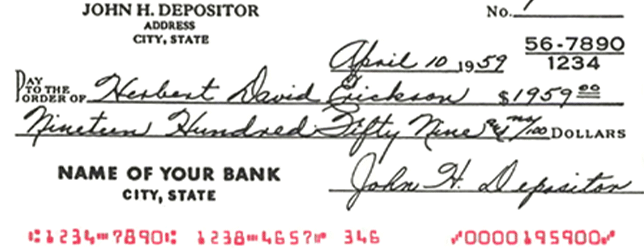

The Federal Reserve also incorporated mechanical “proofing” machines and magnetic ink, which eventually enabled upwards of 100,000 checks to be produced per employee per hour, up from 33,000 checks. Magnetic Ink Character Recognition (MICR) allowed computers to read necessary check information like account and routing numbers.

Source: Federal Reserve Bank of Philadelphia (1964, Off-site). The print at the bottom of the check, highlighted in red, contains the routing number of the bank upon which the check is drawn and the customer's account number.

Current state of Check Services

Although check use has decreased, the average value of a check payment has steadily risen since 2000, so despite a lower number of check payments or the proliferation of faster options for smaller day-to-day transactions, checks remain for transactions such as medical or insurance payments and reimbursements, Collect on Delivery (COD) scenarios, and charitable contributions.